Financial Guarantees expedite and improve funding certainty

The advantages of obtaining a financial guarantee used as completion assurance (not an insurance product) for Completion Assurance Program™ (CAP) funding far outweigh the effort. We will cover any associated costs out of proceeds. A slightly smaller cash deposit can be used instead of a guarantee, also for 100% funding, but qualifying financial guarantees are not usually backed by cash.

If cash happened to be available, minimum ~25% as a deposit, then a guarantee would not be necessary to access CAP funding with flexible and affordable terms. CAP funding is not only more flexible but also much faster, reliable and predictable, with closings typically 30 days or less (upon delivery of either a financial guarantee or proof of capacity for a cash deposit), at these indicative terms.

Project fundraising is largely an artform — with CAP funding security, it becomes more of a science — much more predictable. – Daniel Robin

This matters because the next best option for middle-market project finance (without a guarantee as security or cash deposit) is quite a bit more expensive, takes much longer, and reaching closing is far less predictable.

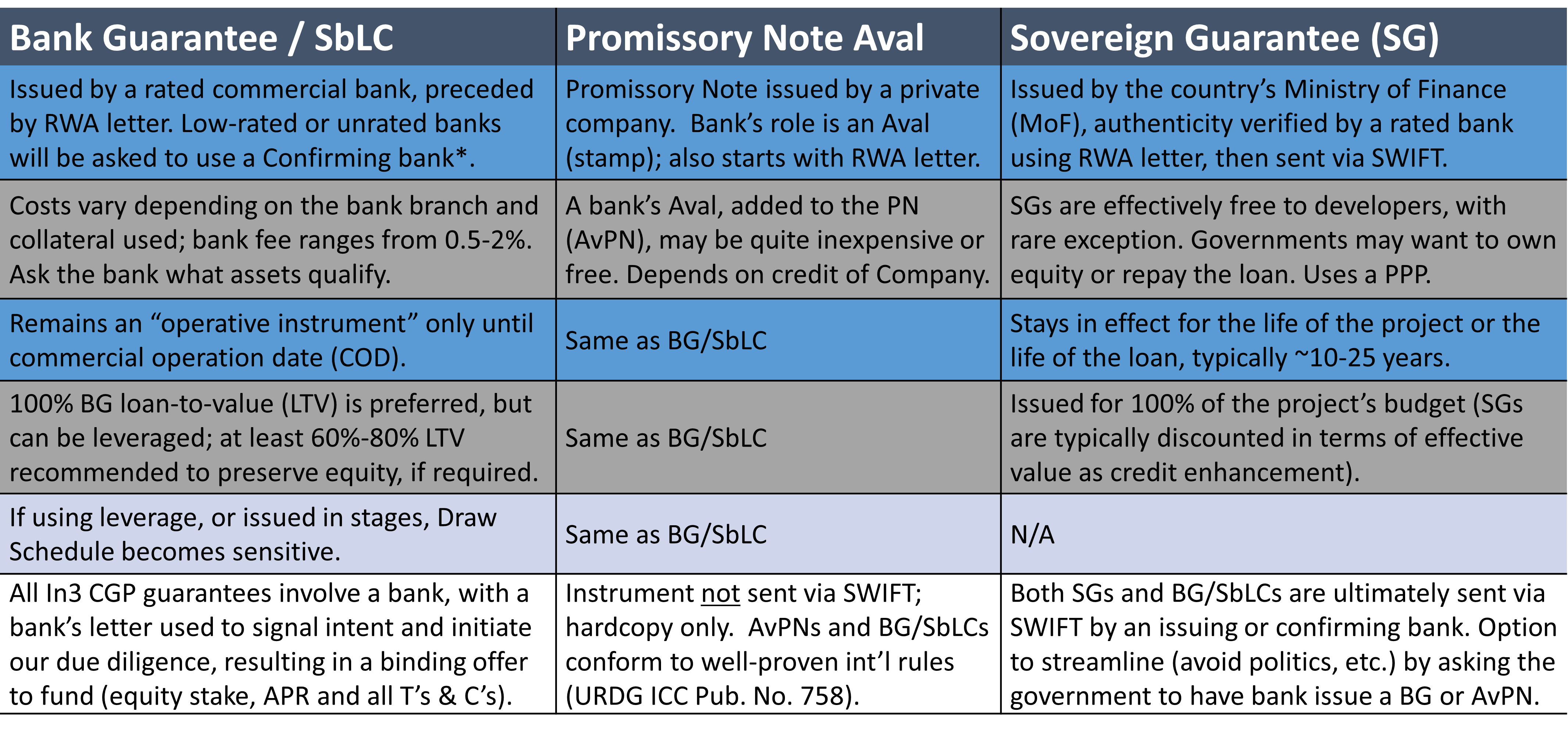

Qualifying for In3 CAP (see summary of requirements) enable us to accept mainly a Standby Letter of Credit (SbLC) backed by assets (complete list of acceptable types), some used directly, or rarely a Bank Guarantee (BG), bank-confirmed Sovereign Guarantee (SG) or bank-endorsed Promissory Note (issued by the guarantor but “avalized” by a bank, an AvPN). How to select and facilitate the right one here.

DEFINITION: What’s the difference between a Completion Assurance Guarantee and …

- Owner cash equity — minimum 25-33% unexpended cash owner equity “skin in the game” can be used instead of a CAG, enabling similarly advantageous terms & conditions as with a guarantee. A CAG is not typically cash, but cash can be used as a deposit, returned upon the last draw, as a streamlined alterative to a financial guarantee. Some developers chose to leverage lines of credit or bridge loans (effectively cash) for this purpose, to obtain CAP funding’s terms and speed of funding.

- Insurance — CAGs are bank-involved, financial instruments, not insurance products. Insurance can be useful for other reasons, including, for example, an EPC’s completion bond, performance bonds, or similar coverage with annual premiums varying from 2% up to 6% or more per year depending on risks mitigated. So far, no bank has converted insurance into an SbLC or any other acceptable financial instrument.

- Financial Guarantees used for Trade Finance — trade finance transactions always use cash collateral to pay the seller; In3CAP CAGs can instead rely on non-cash assets as collateral, depending on what the issuing, confirming or avalizing bank is willing to accept.

- Offtake agreements — although helpful to demonstrate commercial risk mitigation, long-term purchase contracts, such as (with energy) Power Purchase Agreements (PPAs) do not mitigate the risk of project completion. PPAs are a good start, but there’s more to In3CAP funding than having a proven, creditworthy customer. Completion of the project as an operating, revenue-generating asset is key to gaining access to In3CAP’s advantageous terms & conditions.

What are the most common types of CAGs? Main one is a Standby Letter of Credit (SbLC), which is similar to the widely used Bank Guarantee (BG) or Payment Guarantee (PG), or Demand Guarantee (DG). Because our funding is likely to originate from a US bank, however, SbLCs are preferred. BGs are no legal in the US.

Some countries can issue a Sovereign (nation) Guarantee (SG, explained below), or In3’s innovative use of a commercial Promissory Note with a bank’s endorsement (Avalized PN or AvPN).

This comparison chart reveals the similarities and differences of all three options. A few notes about project country location:

{kind=link}

Sovereign Guarantees (SGs) typically do not incur up-front fees for the developer (with rare exception, SGs are free of cost), while Bank Guarantees are issued by either the developer or a private-party sponsor/backer, such as a well-established EPC (Engineering, Procurement & Construction) firm, involved corporation (such as a major equipment supplier) or general contractor hired to build the project, or sponsoring government agency (similar to a Sovereign Guarantee, but from a bank), any of which can offset the bank fees for developers seeking 100% financing. This sponsorship applies when developers have already invested all available capital in organizing and preparing the project for funding.

Solving the 100% funding conundrum

This 100% funding scenario is one of our novel offers — we do quite a bit of qualifying and vetting work, but we do not require any money up front, any “down payment” deposit, or application fee, so there’s really nothing to lose by pursuing this advantageous funding option.

But because banks typically charge from 0.25-3% for their role in sending a BG/SbLC (SGs and bank Avals are usually much less, or free, to well-qualified customers), a sponsor/backer may be needed just to “bridge” that expense. Ask your bank what they will charge to deliver a proposed guarantee instrument per our requirements (download template for them to put in their format here).

The bank’s fee is typically paid to the bank just before financial closing, once all contracts are in place. The sponsor will be reimbursed within 30-45 days after closing, upon first draw, or over multiple draws — whatever arrangement you can negotiate with them.

Sponsor/Backer Incentives

The sponsor may or may not be offered equity participation — up to you. They do need an incentive to bring the guarantee, which can vary widely from a company being hired and paid an “enhanced” fee for their services to a government that stands to benefit from the “social” projects funded by In3’s partners.

At-large guarantors (those not playing a contractor or stakeholder role in the project) probably will want to see an immediate return via a reimbursed bank fee (perhaps plus a margin on top of what they paid the bank) as well as longer-term, minority equity carried interest. This is subject to negotiation with the backer, but we’ve seen 0-20% offered by developers. The developer still manages to retain more than half the rights to cashflows, depending on the guarantee’s coverage.

The sponsor/backer’s exposure in playing this role is nominal — we use the guarantee mostly to screen out fraud and ensure that the funding is used to complete and commission the project. So, assuming the developer is non-fraudulent, there is very little risk of project non-completion. In any case, the backer’s position can be further securitized with a lien against the project assets, and other contractual assurances, as needed. If you wish to involve a sponsor, go here.

Highlights of how to obtain and use a capital guarantee

The rest of this article explains how to obtain and use a Bank Guarantee / Standby Letter of Credit (BG/SbLC), Avalized Promissory Note (AvPN), or Sovereign Guarantee (SG) in financing projects of $25 million or more, and the advantages of doing so through this program.

In3’s approach to expedited funding features best industry practices, backed by a well-organized program and US Family Office partners with a strong track record of success in both developed and developing countries worldwide. Ask your In3 Affiliate to assist with arranging a pre-qualified project funding proposal using In3Finance’s Proposal Builder or preview the Stepwise Guide to fundraising success with CAP.

- We operate globally, but depending on where you are working (In3 list of qualified countries), there may be differences in what type of funding security is available. Bank size is not usually an issue.

- A BG is effectively the same as a Standby Letter of Credit (SbLC) in the US and some other markets, but …

- Sovereign Guarantees (SGs) are only available when a sovereign government (the Minister of Finance) will authorize it as part of public/private cooperation. SGs can be tricky, depending on the government itself and access to the appropriate government contacts. Not all governments issue them. They’re helpful to emerging or frontier markets, and certainly developing countries, but politics can get in the way.

- BG/SbLCs and AvPNs, by contrast to SGs, can be obtained anywhere.

See chart below to summarize and build on these points:

Bank Guarantees or Avalized Promissory Notes can be arranged with a bank when either the developer has an existing relationship with the selected bank or a “Sponsor” is invited to ensure completion of the project using whatever the bank requires as collateral (an asset that is temporarily “blocked” using the aforementioned BG/SbLC instrument, or relying on the credit rating of the customer requesting an Aval on In3’s simple Promissory Note), plus sufficient capital available to cover the initial costs of obtaining the instrument from the selected bank, if any.

It is quite possible to establish a new relationship with a bank for the sake of this capital guarantee, just allow for the usual Know Your Customer (KYC) formalities, which take additional time.

Bank fees vary widely; ask your bank, or suggest that a prospective Sponsor ask theirs. The “Aval” is probably least expensive for qualified customers of the bank, where “qualified” means that the requestor’s credit rating or credit history is reasonably strong. Larger, stronger banks are the better choice, but usually charge more for their services. Keep in mind that we can reimburse bank fees from funding proceeds, shortly after closing out of initial draw(s).

For smaller banks, check their credit rating (we use Moody’s). The bank fee is only needed to begin the process, and the bank’s instrument only remains in place during the project construction period (until Commercial Operation Date), after which the BG/SbLC or AvPN is allowed to expire. If necessary to renew the instrument (often issued annually) any subsequent fees or bank “margin” can be paid for or reimbursed out of loaned/invested proceeds.

History shows that experienced Developers have been successful at involving a well-established Sponsor (usually a contractor/stakeholder in the project itself) to leverage the sponsor’s asset base to transfer the bank fee responsibility to the sponsoring company in exchange for incentivized compensation for doing their part in designing/engineering, integrating, major equipment supply and/or construction the project, as described above. Request our presentation materials on this topic for further specifics.

Can you leverage a guarantee used as completion security? Yes. BG/SbLCs or AvPNs can be leveraged, with as little as 30-35% coverage (for example, if seeking $100M in total funding, the instrument’s face value could be as low as $30M-$35M), though we do seek a larger equity carry for the uncovered portion of the loan. More on this advanced topic here.

Why bother obtaining a guarantee at all?

This pathway to project funding is worth careful consideration because the economic and practical benefits of using either an SG or BG far outweigh the time, effort or costs involved. Funding via this pathway is …

- affordable — 3% (SONIA + 2.5% fixed) APR for the life of the loan, preserving owner equity to the maximum extent possible

- reliable/predictable — once a project is pre-qualified, which we offer without any risk or obligation to the developer, the odds of reaching financial closing is extremely high

- relatively fast — 2-4 weeks to closing, with first draw 30-45 days at most after closing; traditional project finance Due Diligence can surface all kinds of unacceptable risk as perceived by the funding underwriters, where few projects ever realize financial closing even after many months of good faith back-and-forth, and

- In3’s program offers flexibility to finance up to 100% of the project, with funding available at any reasonable stage of development, without our partners asking for control.

Perhaps most importantly, CAP solves these 4 notorious problems with traditional project finance — the need for certainty, speed, 100% financing at reasonable terms and aligned incentives that help secure the funding in the first place.

How is this different from traditional project finance?

We like to say our pathway to funding is “faster, easier, and better.” Click on this comparison chart on the right for a summary of the differences between our family office’s program in contrast with traditional project finance.

How does the program work?

We are quite systematic and organized in our approach, so please do your best to understand and carefully follow our procedures. We welcome clarification questions at any time.

Stage 1: Screening and pre-qualification – In3 & partners assess if the project(s) are investable – basis: quality and size of the capital guarantee(s), rating of the issuing bank, financial fundamentals (including unlevered IRR), commercial risk profile, principals & ownership.

See our 9-step guide to success with CAP funding

- Send first 4 of the Six Essentials along with collected documentation to In3 (NDA available), starting with a rated bank issuing an RWA Letter (“ready, willing and able”) to begin the transaction with our partner receiving bank, then the package of materials can be pre-approved for funding, following by the actual instrument, BG/SbLC, AvPN or Sovereign Guarantee. Either a BG, SbLC or AvPN guarantee instrument would be sent via Brussels SWIFT after entering the financing contracts*.

- In3 audits and determines roles, scope of work, and enters agreement(s), then delivers project (or portfolio of projects) to in-house lender/equity partner.

- Gain initial approvals within 15 days; if accepted, closing within ~30 days with Sovereign or Bank Guarantee/SbLC. First draw per development/construction schedule. More on Sources & Uses statements and draw schedules

Stage 2: Our due diligence — takes no more than 30 days, once the file is pre-qualified and approved per above.

Stage 3: Launch & Fund — enter funding contracts, deliver guarantee instrument, and begin monthly draws. Proceed until project completion and commissioning, at which time the operative BG/SbLC would normally be allowed to expire.

See our 1-page protocol (PDF) — process steps “from Inception to Closing”

Recommendations for obtaining a Capital Guarantee

See our tips on “how to” obtain a guarantee at In3 Finance.

In general, start by first considering what party or parties have an interest in the project such that they could be willing, if properly approached, to issue a capital guarantee, such as governments (Ministry of Finance only) for SGs, or to post a Standby Letter of Credit (SbLC) on behalf of the project using a Bank Guarantee memo called MT-760, which can be sent directly from one bank to another via the SWIFT system*.

Second, select a major bank, usually one with a reasonably strong credit rating, such as (ideally) a top 25 international bank. Such banks will have already registered via SWIFT RMA or RMA Plus. Central banks or national banks (some with US or European affiliates) may or may not have the asset depth needed for major infrastructure projects. The selected bank does not need to be local to the project. Top global banks are preferred, but not required.

How to select an appropriate bank to issue the guarantee instrument

Our partners rely on a network of relationships with hundreds of banks. Smaller banks can be acceptable in the US and other markets for larger projects ($75 million and above), and can justify establishing a new relationship, and also enable us to overlook a bank’s less-than-perfect credit rating. Smaller projects are more difficult to justify. We prefer Moody’s for bank credit ratings. In some cases, an additional bank can serve to “confirm” (backstop) a smaller or low-rated issuing bank’s BG/SbLC. Confirming banks are usually among the Top 25, such as Citi, Chase, Barclays, Deutsche, etc.

We also ask for confirmation of a Sovereign Guarantee so that it can be sent to us by the confirming bank, initially using MT760 SWIFT.

Finally, a copy of the SG or BG/SbLC language to be used in the SWIFT notice should be sent to us for pre-approval . This is recommended because the wording does matter (ask us for a template of sample verbiage), then the actual BG/SbLC will always be sent via SWIFT MT-760 to our underwriters to complete the transaction. The process begin’s with a bank’s letter of intent known an an RWA Letter (“ready, willing and able”) to confirm that the actual instrument will later be sent once all contracts are in place, per financial terms and conditions established at that time.

RWA Letter and SbLC/BG verbiage templates available upon request.

* SWIFT provides a secure network of ~10,000 financial institutions in 212 different countries. These SWIFT-registered institutions reliably send and receive information about their financial transactions. More at swift.com

See the protocol steps for Bank Guarantees or for Sovereign Guarantees

What makes using a capital guarantee worthwhile?

See our investment terms & conditions for the quantitative aspects of an acceptable project or portfolio to be financed — minimums do apply. We call this our Completion Assurance [Guarantee] Program (CAP funding) with four basic “S” cornerstones — size ($25 million or more), space (more than 30 qualify), stage (almost any — no need to be shovel-ready) and surety. More on guarantees used as credit enhancement

Project finance benefits from having a bank take on the risk of default as that makes due diligence far less onerous and thus the terms, requirements and timing far more predictable. We will usually close on projects that have a Loan Guarantee sent via SWIFT within 30 days.

The above information is part of our briefing materials, available to qualified project developers and their authorized agents for review. Visit In3 Capital Partners project finance Tools and Resource Center or the In3 CAP Funding Overview for further details.